In my article dated 30th Nov’2015, I had advocated investments in debt funds as an alternative to FD. Throughout 2016, we had advised investors to move out from gilt and invest in accrual products as the yields had come down to abysmal lows of 6.50% to 6.20 % without a commensurate reduction in rates by RBI.

RBI policy announced on Feb 17, resulted in Yields crashing down, thereby somewhat realigning the yield to more practical rates of 7 to 7.2 % approx.

The current FD rates are 6.75 to 7.0% pa.

In the near future, if the interest rates do not rise (unlikely), it would be wise for investors to park money in Short term/long-term debt funds (depending upon investment horizon). The immediate question is, what is the advantage?

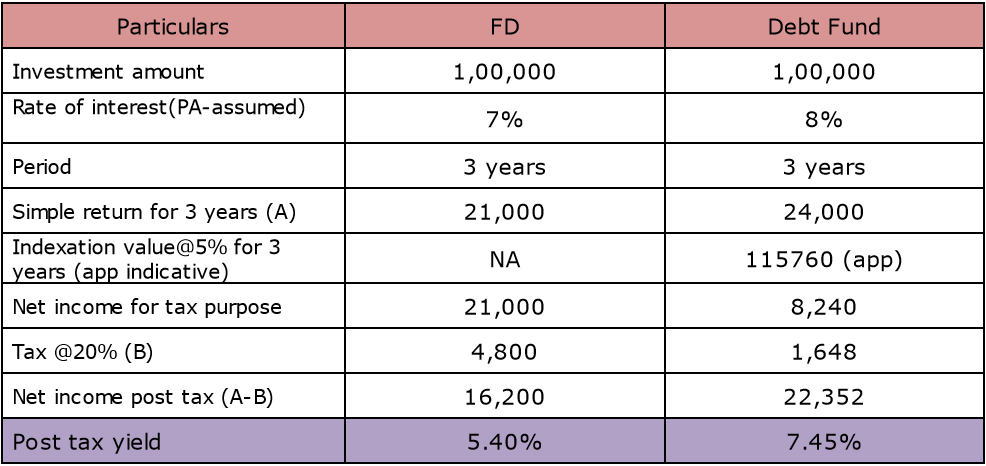

The main advantage of this investment is Tax benefits. I illustrate as below:

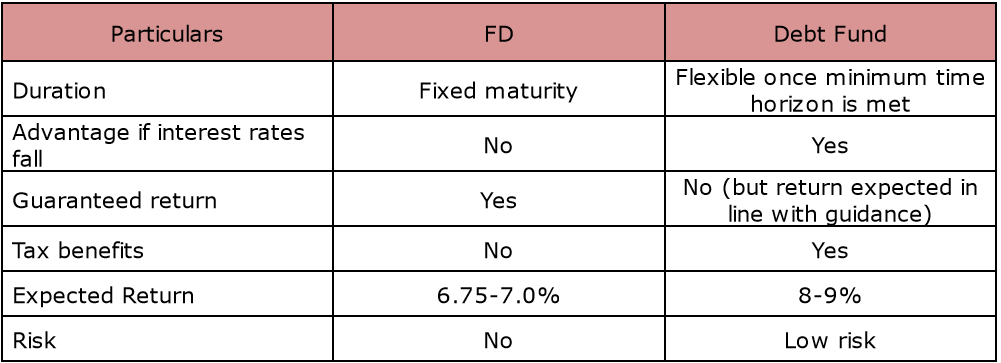

Apart from the Tax benefits that we derive, the other Pros and cons of investment in MF debt Scheme is elucidated below:

In view of the above, I believe that it would be a prudent move for investors to invest through MF debt schemes rather than FDs.

With warm regards,

Samrendra Tibarewalla, CFPCM

PS: You are the best manager of your money. Please take informed decisions only.

Disclaimer: The author in no way will be held responsible for losses incurred on the basis of the above recommendations. The investors are advised to take independent decisions after verifying all facts.

FAQ: Debt Funds vs. Fixed Deposits

1. What happened to yields following the RBI policy announcement in February 2017?

The RBI policy announced in February 2017 led to a crash in yields, realigning them to more practical rates of approximately 7 to 7.2%.

2. What could be the future of interest rates, and how should investors react?

If interest rates do not rise, which is unlikely, it would be wise for investors to consider parking their money in short-term or long-term debt funds, depending on their investment horizon.

3. What is the main advantage of investing in debt funds over FDs?

The main advantage of investing in debt funds over FDs is the tax benefits, which can significantly enhance the effective returns for investors, especially those in higher tax brackets.

4. Would investing in MF debt schemes be a prudent move for investors?

Based on the analysis, investing through MF debt schemes rather than FDs is considered a prudent move, especially considering the potential for higher after-tax returns and the flexibility offered by debt funds.